.svg)

Plaintext Quarterly - Choppy Waters, Clear Skies

The first half of 2024 was constructive for crypto markets. The launch of the wildly successful Bitcoin ETFs and the approval of the Ethereum ETFs led to a 70% price increase for both BTC and ETH. The political headwinds have taken a turn as Trump chose to counter the Biden administration’s hostile view towards crypto by making support for the industry a cornerstone of his campaign. SAB 121, a bill that restricts the ability for banks to custody crypto, was overturned by Congress but vetoed by Biden. FIT21, which proposes reasonable regulatory guardrails and limits the SEC’s power over crypto, made it through the House, signifying a shift in sentiment. And, of course, the Bitcoin Halving took place at the end of May.

Despite the positive progress and YTD price action, the current sentiment is atrocious. Choppy markets test the patience of crypto investors more than anything. ETF inflows were simply priced into the market during Q1, and derivatives data shows that traders got ahead of themselves. The options market had a spike in IV, open interest, and skew in March, which marked the beginning of the choppy markets.

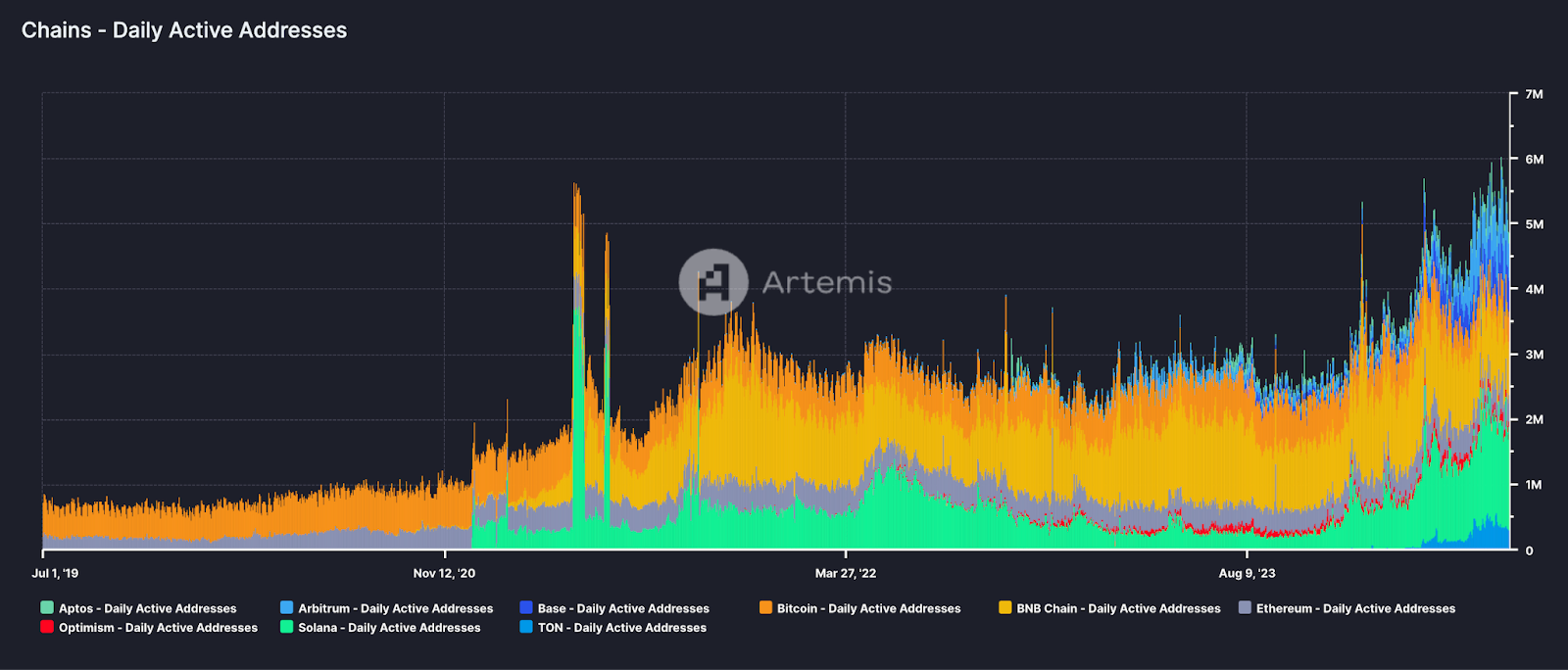

Amid the choppy market, people have lamented the lack of breakout use cases. I disagree with the premise; Bitcoin is now a true gold competitor on the global stage, DeFi proved to be revolutionary and is now onboarding the biggest financial institutions in the world, and stablecoins are facilitating enormous cross-border payment volume. Crypto is more inevitable today than it ever has been. But to address the negative sentiment, I think there’s a misplaced expectation that liquidity cycles and technology cycles should align. Bitcoin’s halving occurs every four years, and global markets have also coincidentally experienced mini-liquidity cycles every four years.

In parallel with these liquidity cycles, tech innovations have also led to a surge in new crypto opportunities. In 2016-2017, Ethereum and ICOs promised new forms of capital formation. Investors’ imaginations ran wild with all the ways Ethereum could be used to disrupt incumbent businesses. In 2020-2021, decentralized finance found product market fit by facilitating trillions in peer-to-peer exchange and lending. Liquidity and tech breakthroughs have coincided in crypto over the last two cycles, so people expect the trend to continue.

The reality is we’re in an upward liquidity cycle, which is pulling crypto prices higher and will likely continue to do so, but maybe the tech innovation won’t perfectly overlap with this liquidity growth. These cycles don’t need to match, and expecting them to do so is unrealistic. Tech doesn’t move at the pace of M2 growth or with fluctuations in interest rates. What is important to remember is that crypto’s superpower is global capital coordination, and we’ll continue to see new use cases. Breakout adoption might happen in RWA protocols, lending, stablecoins, gaming, DePIN, music, or something entirely unexpected, but it’s a matter of when not if.

Staying attuned to the market is crucial to 1) leverage the clear liquidity trade while 2) recognizing when new tech paradigms emerge. As an example, last year, if you had recognized the role crypto could play in AI, there were multiple ways to take advantage. It’s much easier to allocate to trends as they emerge than it is to predict them.

Buy Boredom

Sentiment is easily predictable in crypto. When prices go up, everyone is interested and relatively happy. When prices are sideways and down, people are miserable, and investors divert their attention to just about anything else. Bitcoin has been sideways for four months now. Altcoins are down over 50% in many cases. New allocators have slowed their investments in crypto funds. Crypto Twitter is a wasteland. Mt. Gox distributions are beginning shortly, the US government has been selling Bitcoin seized from Silk Road, and the German government has been selling their own supply of seized Bitcoin. There are a lot of “easy” reasons to be bearish. The prevailing sentiment is that crypto is poised for a rocky few months, but the long-term trend is higher.

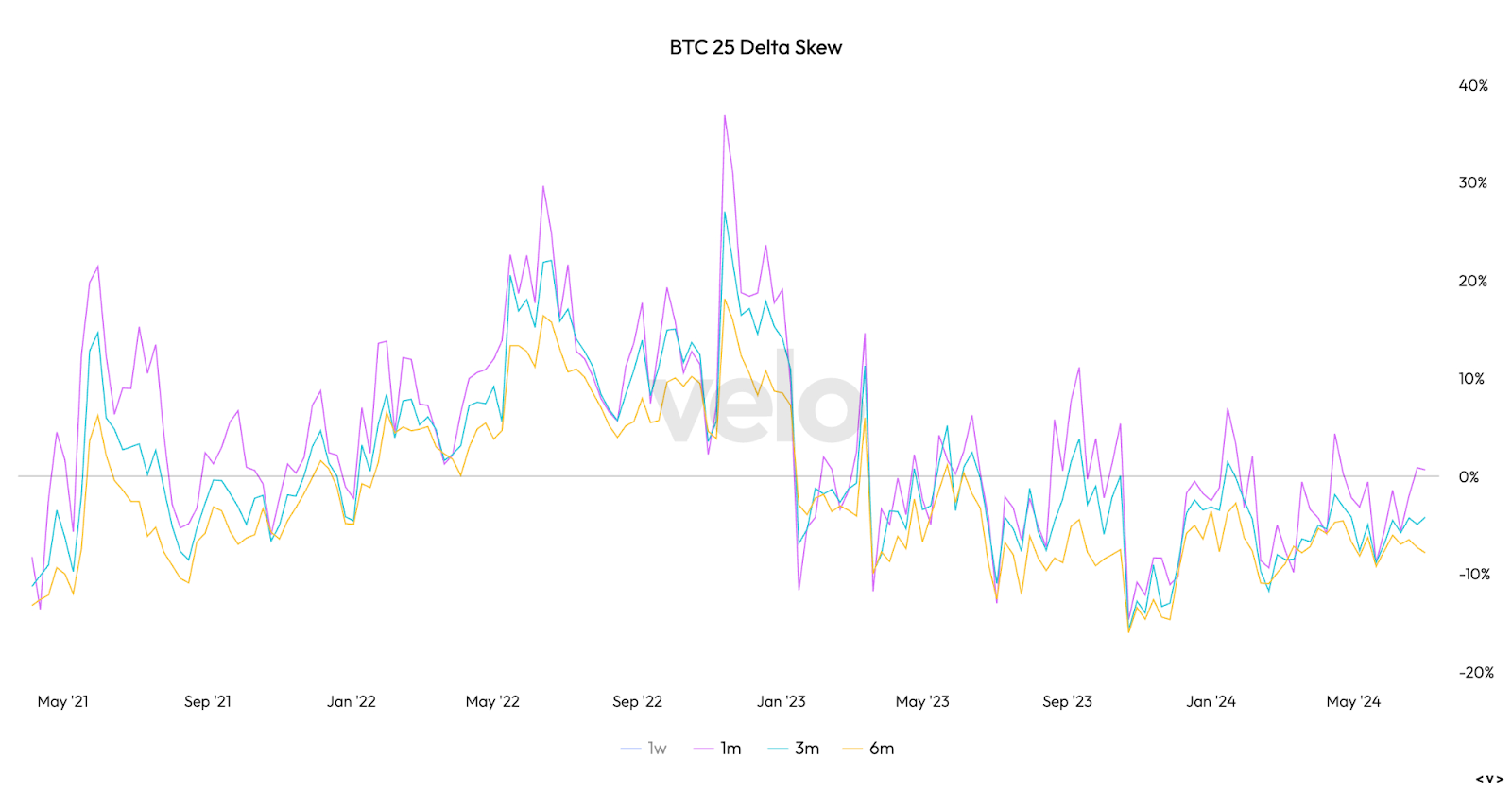

This sentiment is visible in the options skew and the term structure below. The short-term (1-month) skew is positioned more defensively than the long-term (6-month) skew. The market is betting on short-term weakness and long-term strength.

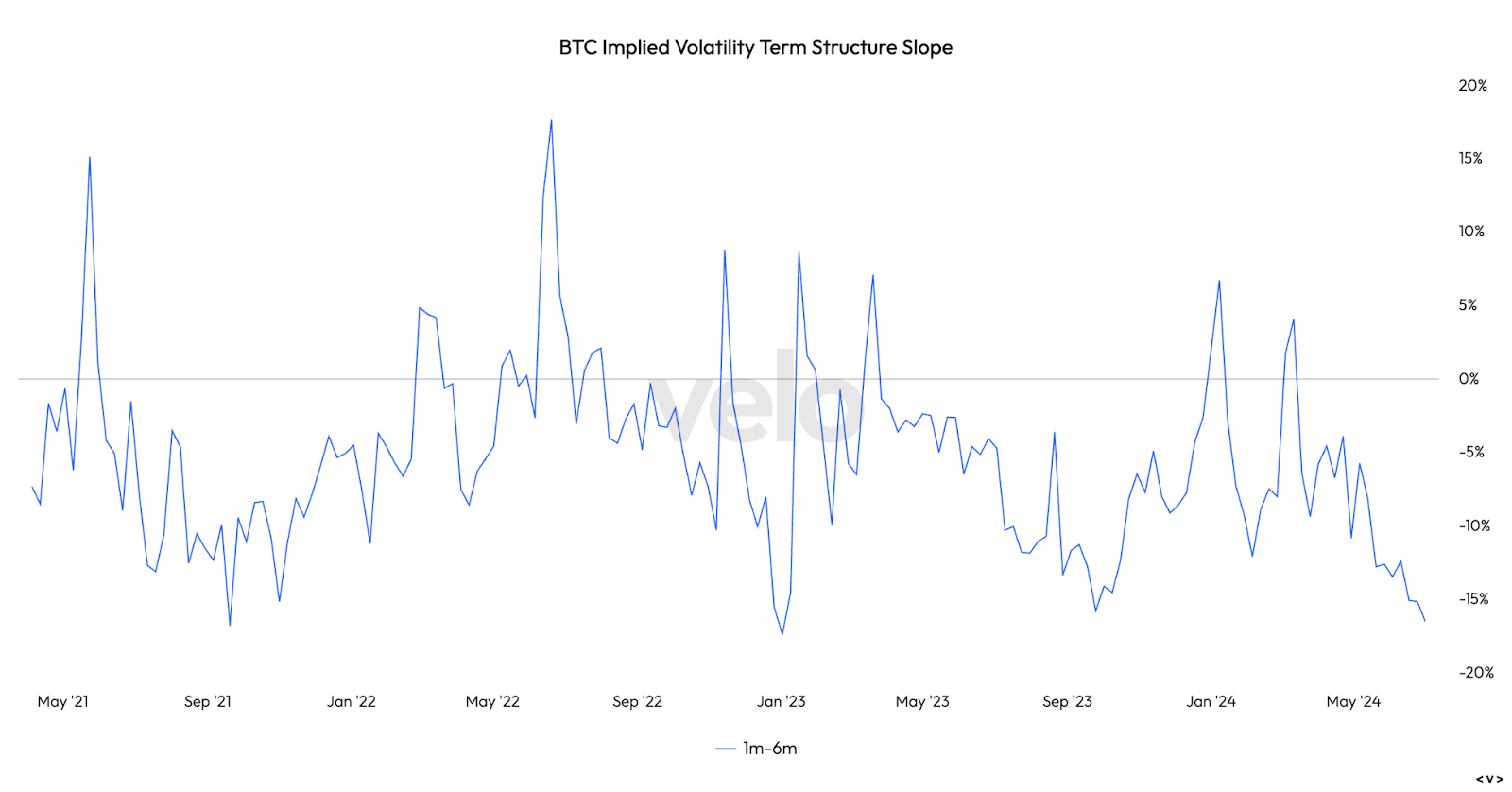

This can also be seen clearly in the volatility term structure. 6-month volatility is far more expensive than 1-month volatility. Notice the last three times the reading was this low - September 20, 2021, January 2, 2023, and September 25, 2023. In the month following each event, Bitcoin went up 40%, 40% and 28%, respectively. Currently, the market has fallen asleep and is ignoring the potential for an enormous move in the next few months.

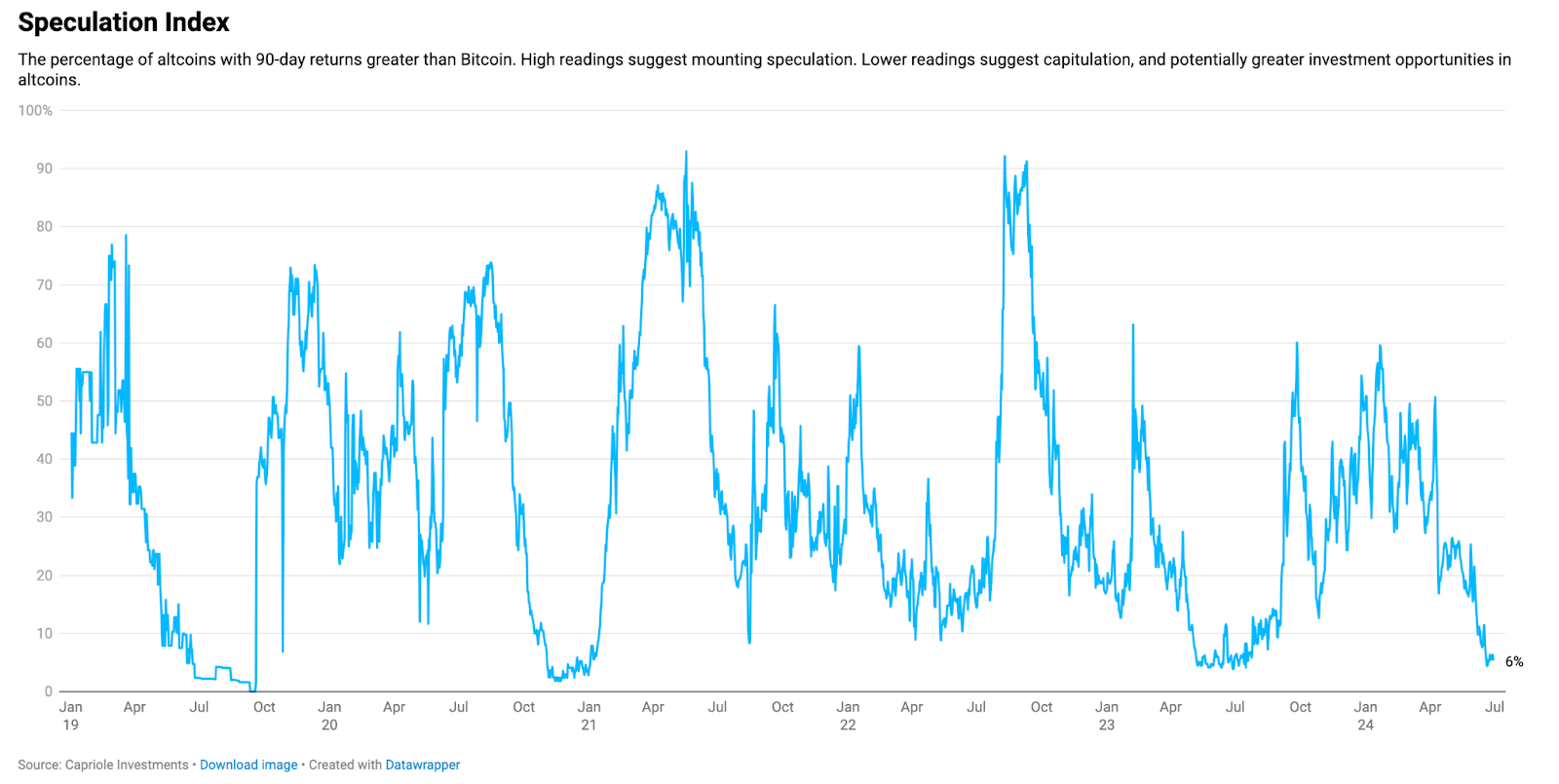

Sentiment around altcoins has rarely been poorer, and with good reason. Over the last three months, only 6% of alts have outperformed Bitcoin. This recent trend has led many to believe altcoin outperformance is a relic of the past. I strongly disagree. For one, crypto is wildly reflexive because it’s so inherently financial. The fundamentals of altcoins lag price. DeFi is the best example of this. As prices rise, trading volume and collateral amounts increase, bringing more revenue to DeFi protocols. It’s only a matter of time before we see huge outperformance in alts. If everyone is already positioned defensively on alts, then there aren’t many marginal sellers to keep pushing down prices.

But not all altcoins will outperform. There will continue to be high dispersion in the crypto markets because so many assets are emerging daily, cannibalizing weak performers. We’re focused on two distinct approaches:

- Find asymmetric liquid opportunities at the very early stages. Last year, we used this approach to identify projects in the AI space, such as Bittensor and Nosana, and consumer projects like Sanko Game Corp.

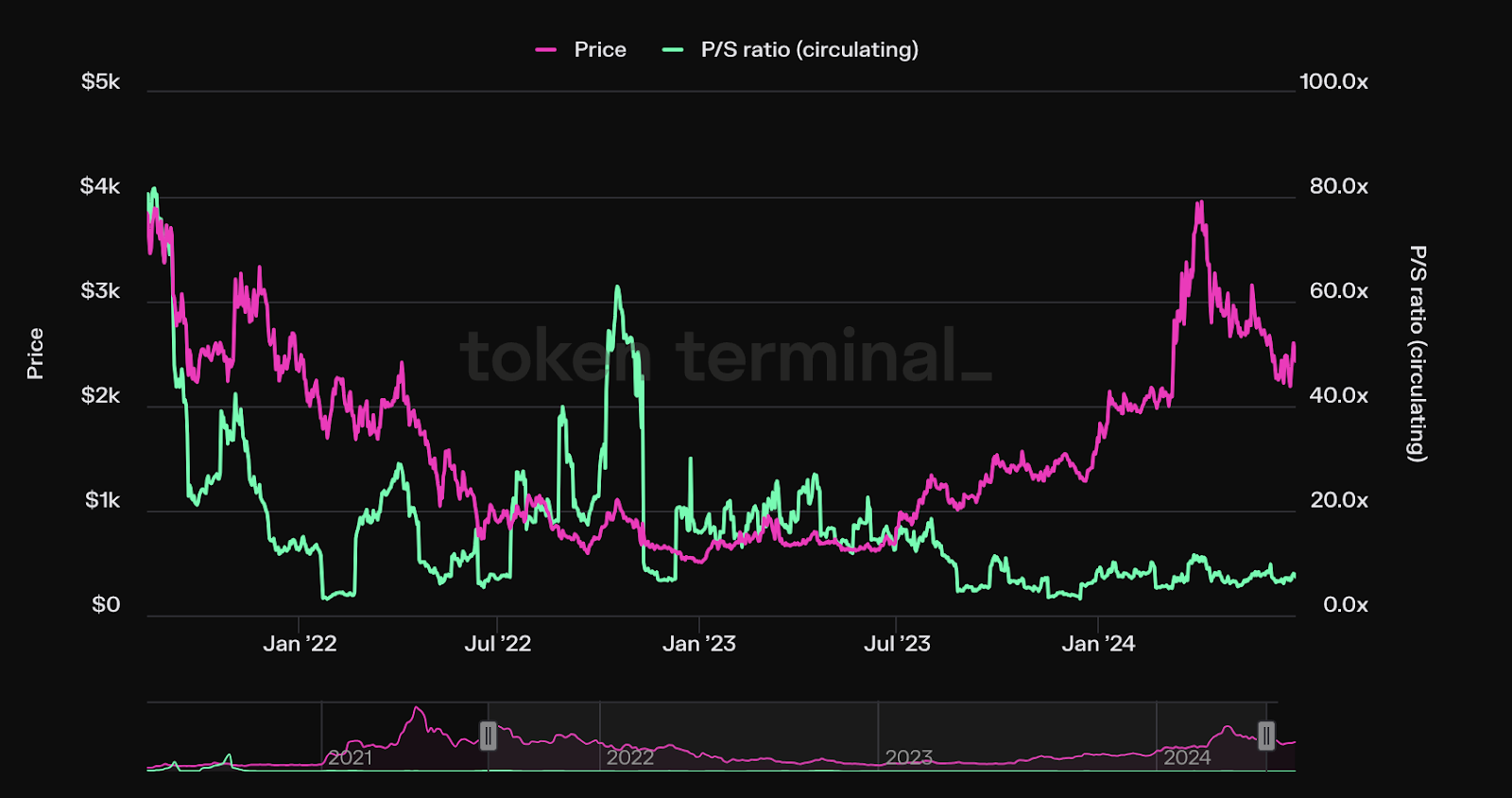

- Identify assets that have found product-market fit and demonstrate sustainable growth. Solana and Maker might fall into this bucket; they’re well-known but are market leaders in their respective categories with positive trending metrics. In general, the DeFi market offers some attractive opportunities, given how cheaply priced projects are now relative to their revenues. The chart below shows Maker’s price-to-sales ratio of 7.3 despite a major price jump over the last year.

We continue to keep a close eye on consumer applications. Our thesis is simple: all else equal, a crypto app is better than a non-crypto app. The problem is that all else has not been equal up until now. The UX of most crypto apps is poor, to say the least. But this is changing. For example, Nina Protocol is the easiest place to publish and purchase music; sign in with email, pay with a credit card, and in minutes, you have a song stored to Arweave forever. Now, Nina has a mobile app where fans can easily listen to their favorite songs. We’re just now seeing UX parity with web 2.0 apps, and it’s very exciting.

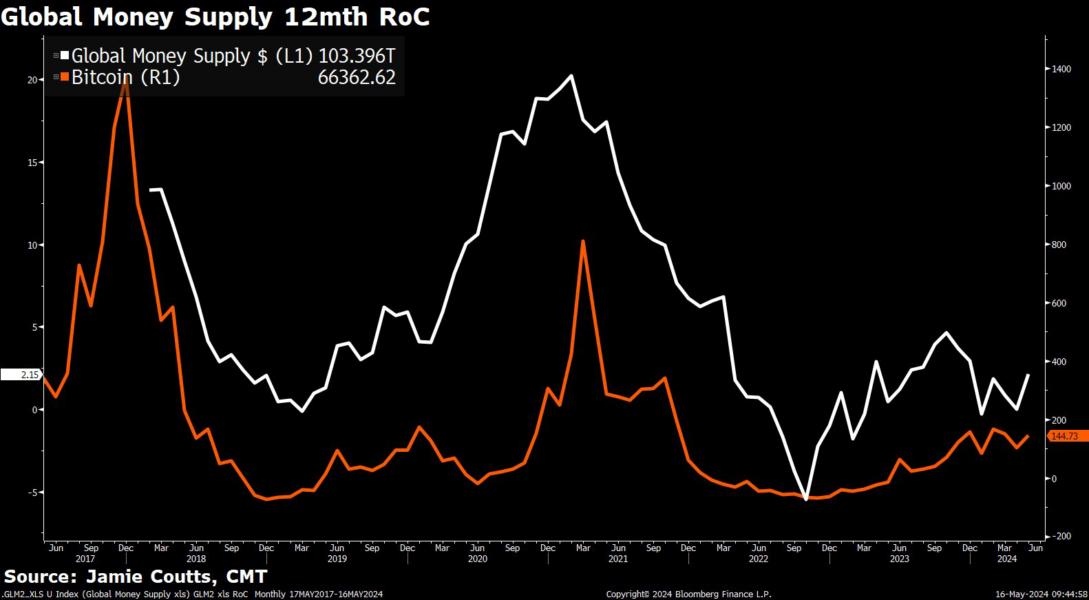

On the macro front, CPI is now hovering around 3% after peaking at 9%. Where inflation heads from here is anyone’s guess, but the Fed can claim a partial victory so far. If unemployment spikes, credit tightens, or there’s some other volatility-inducing event, the Fed has wiggle room to support markets. More importantly, fiscal spending is one-directional, so it’s hard to be a bearish crypto in light of the other tailwinds mentioned above.

Summary

Q2 shook out weak hands. Choppy waters have tested the market’s patience. Despite the Halving, major regulatory progress, the ETH ETF approvals, and positive fundamentals, the sentiment suggests the “cycle” is over. The best time to pay attention is when nobody else is. Prices and volatility are cheap, and the ecosystem continues to march forward. Sentiment might be poor right now, but blockchain use has never been higher.