.svg)

Plaintext Quarterly - 4Q24

Gold is having its best year on record, the Fed is starting its easing cycle, China is beginning aggressive stimulus, Bitcoin has been ranging for seven months while absorbing an enormous amount of irregular supply, current derivatives positioning is bearish, and Q4 seasonality is historically very positive for crypto. The setup is about as good as it gets.

Macro

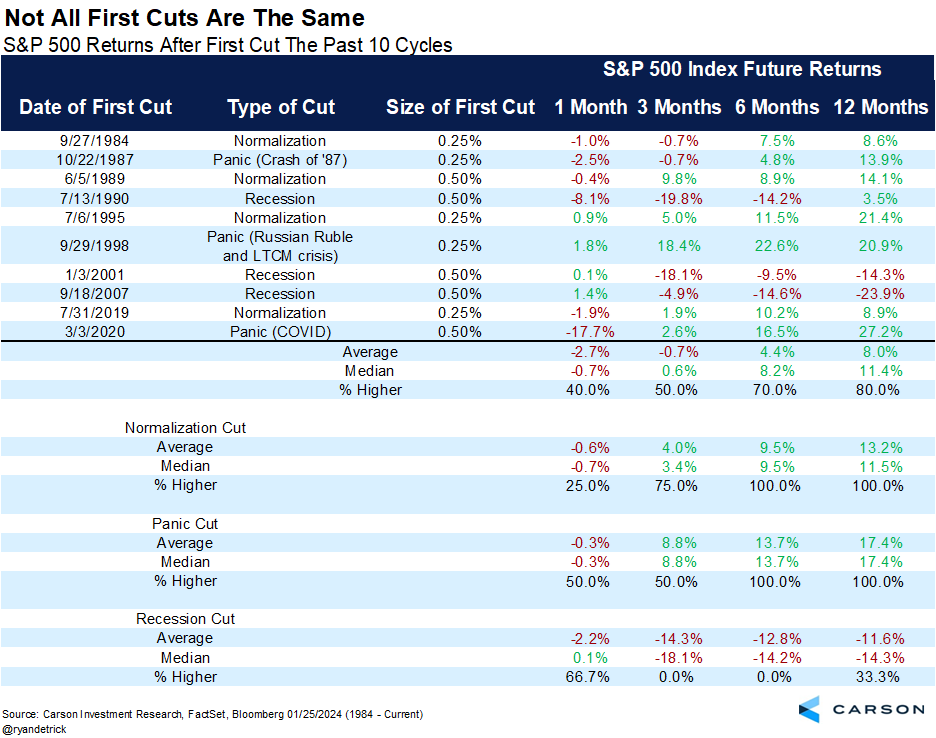

The question of the hour is: Are rate cuts bullish or bearish? History tells us that it depends on whether we enter a recession. Looking at the table below, the market has shown poor forward performance when the cuts aim to lift us out of a recession. When the cuts are to normalize monetary policy, forward performance has been excellent, with the S&P 500 13.2% higher twelve months after the first cut, on average.

Are we heading into a recession? Unemployment has ticked up to 4.2% but is still near historical lows, and jobless claims have trended downward in the last two months. Nominal GDP growth is 5.7%, and real GDP is 3.0%, indicating a healthy and growing economy. The personal savings rate is at historically low levels, which might give pause for concern if financial conditions tighten, but the opposite is happening. The Fed just began its easing cycle, and deficit spending is 6% of GDP. There are concerns below the surface but fiscal and monetary policy will provide the necessary fuel to keep the market happy for the next six months.

The real risk lies six to twelve months out, when we see what effects the current policy has on inflation. If inflation begins ramping up, there will be cause for concern, especially considering the personal savings will be near historical lows and the labor market won’t be as strong as post-covid. Until then, the conditions are extremely favorable for risk assets. The two largest economies in the world are easing financial conditions, which will push investors search for higher returns.

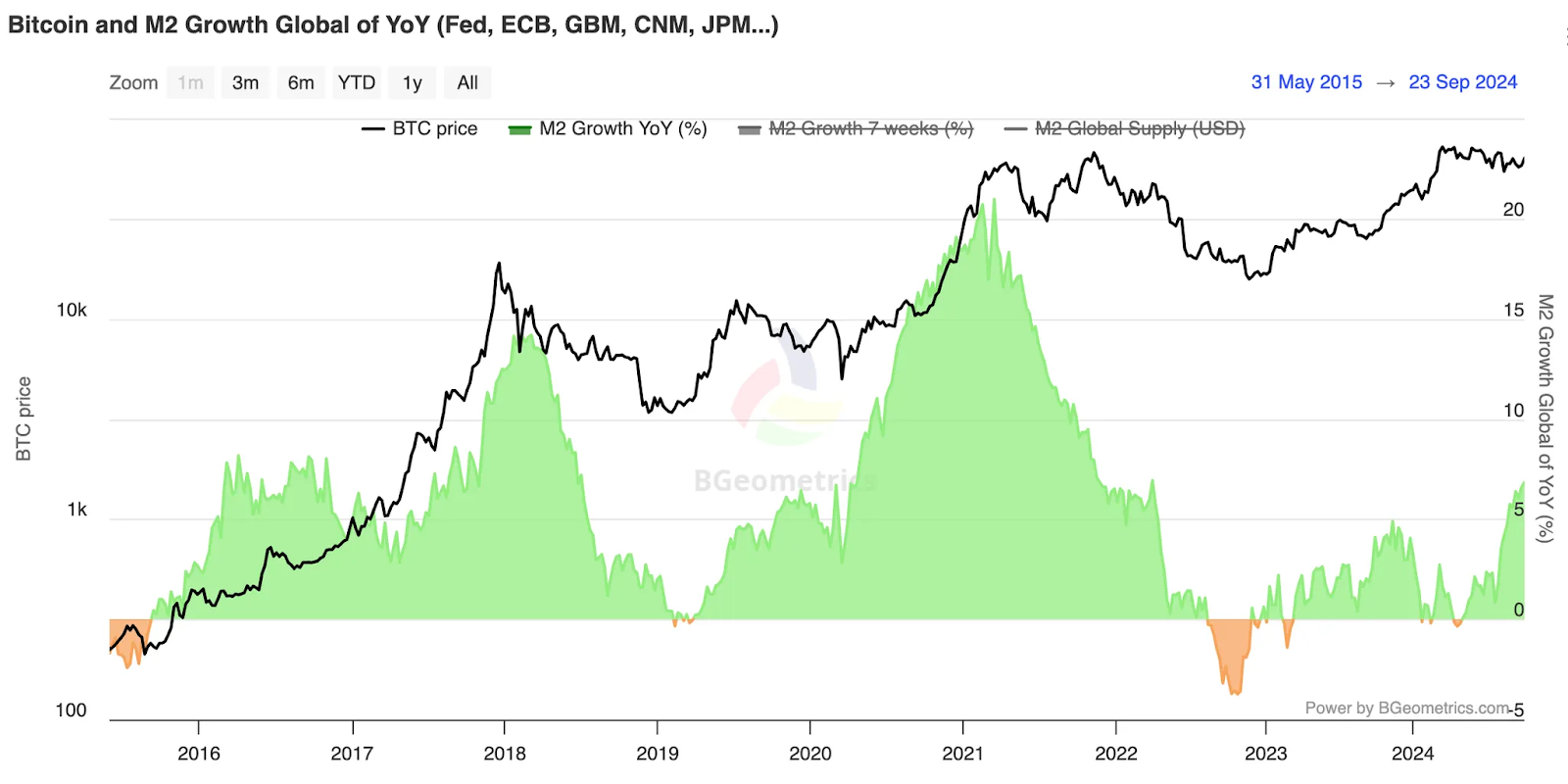

M2 and global liquidity have begun accelerating in the last two months. Investors should aim to allocate to the fastest horse in these types of conditions.

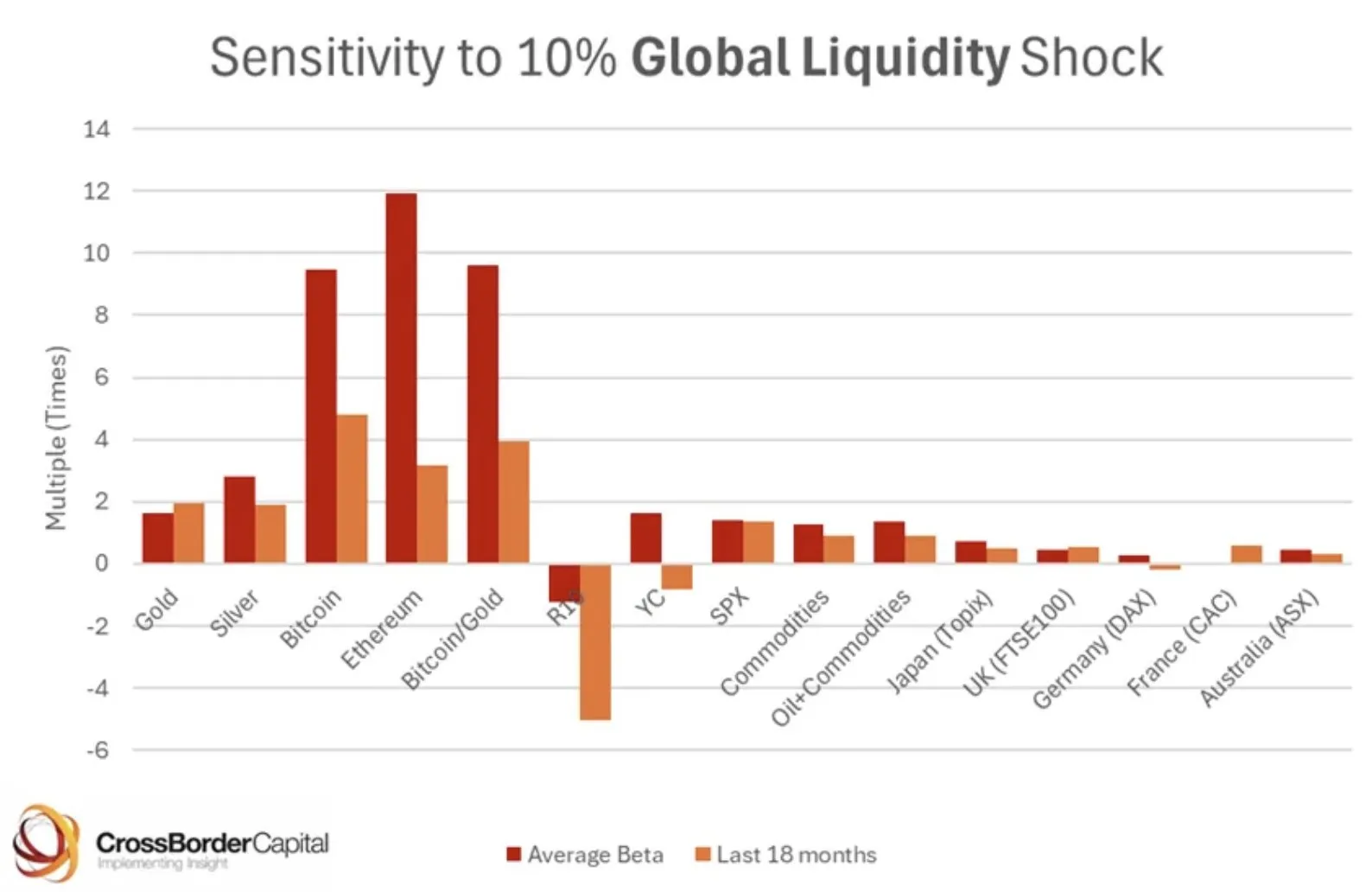

The chart below supports the conclusion that Bitcoin and the crypto asset class are the fastest horses when M2 and liquidity are growing. With a 10% shock to global liquidity, Bitcoin and Ethereum have shown to be the most sensitive assets as measured over the last eighteen months.

Bitcoin

Bitcoin has been been consolidating for seven months after the much awaited ETF approvals and the Bitcoin Halving. We believe it’s on the verge of an enormous rally. As “digital gold”, it’s striking how closely Bitcoin’s chart looks to gold’s. Bitcoin’s pattern is just playing out in three times faster. Gold has recently reacted to the surge in global liquidity and Bitcoin will be soon to follow.

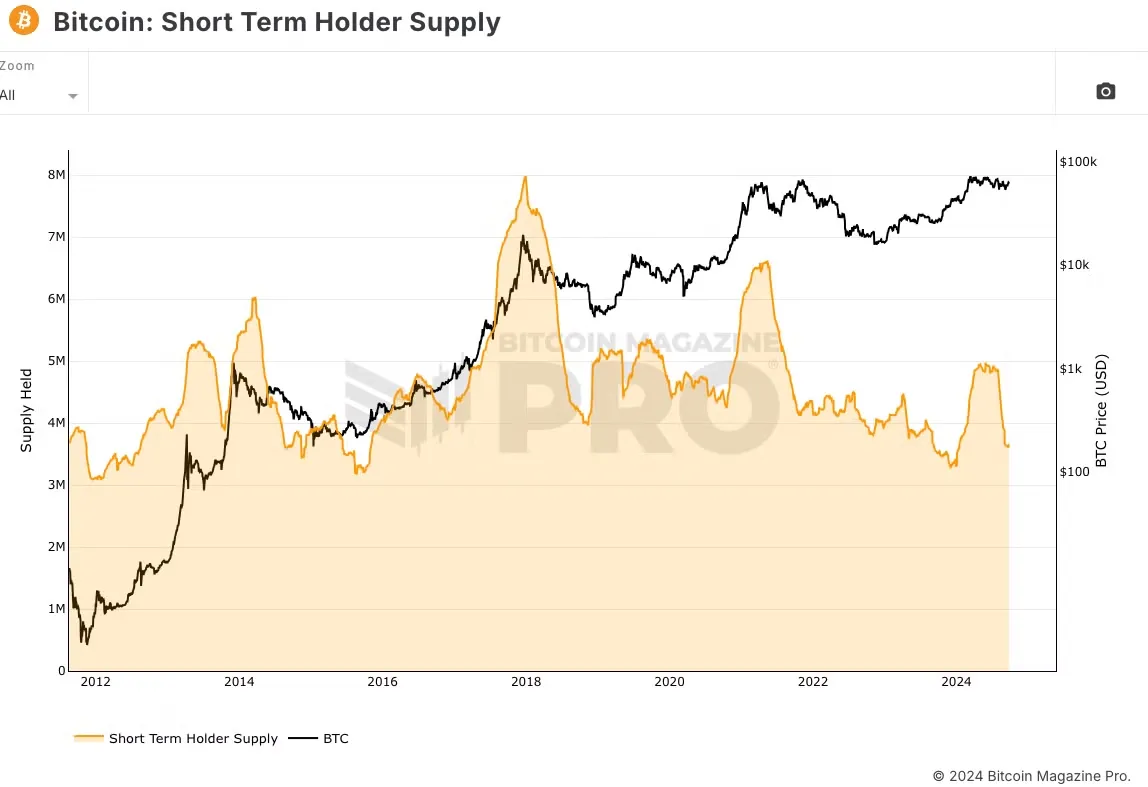

The ETFs allowed GBTC holders to finally get liquidity. We can see this in the spike of short term supply in January. Short term supply is now near the lowest it’s ever been, historically a very good indicator of future direction.

Importantly, positioning is neutral given how constructive the setup is for Bitcoin. 6 month skew is positioned bearish relative to recent history. Being bullish here actually appears to be contrarian.

**\

Altcoins**

Most of the time, altcoins underperform Bitcoin. But there are brief periods when the outperformance is so enormous that it more than makes up for the periods of underperformance. We are on the brink of that period when good asset selection can lead to outperforming Bitcoin by many multiples. This chart of long-tail alts relative to BTC shows early signs of a trend change.

The Russell 2000, or the traditional market’s “altcoin index”, looks like it’s on the verge of breaking out relative to the S&P 500. The last time it did this, Bitcoin broke to new highs and altcoins like Solana went up thousands of percent.

If alts are due to outperform, where will the outperformance come from, specifically? The most interesting areas of crypto are the AI sector, DePIN broadly, and DeFI. Within the AI sector, we think data curation, GPU networks, training and inference, and agents are all areas that will do well. Data curation is a particularly important and overlooked segment of the AI market; data is likely to be a bottleneck for bettering AI, and decentralized networks have a unique advantage in data collection.

While AI x crypto projects are early in their adoption cycle, DeFi is much further along. DeFi represents the sector with the best PMF in crypto. These projects have a lower ceiling than some of the newer, sexier opportunities but also offer a high probability of success. The sector has underperformed for three years and is generally under-owned and under-loved.

Conclusion

Rising liquidity and lower rates will force investors to move up the risk curve for outperformance. Investors who have avoided Bitcoin will pile in. Investors who have ignored altcoins will quickly be reminded of promising new use cases in the crypto market because, as always, narrative follows price. Nothing is ever certain in markets, but the current setup for crypto is outstanding.